What Is a Good Cost Per Acquisition? a DTC Guide

By Arthur Falcone · Founder of Arlo

You open Meta Ads, Google Ads, and Shopify on three tabs. Spend looks manageable. Orders came in. ROAS on one campaign even looks strong. But you still have that uncomfortable question in the back of your head: did those customers make you money, or did you just buy revenue at a bad price?

That tension is where most DTC operators live.

The problem usually isn't that founders ignore cost per acquisition. It's that they trust the version handed to them by ad platforms. That number can be useful, but it's often a vanity CPA. It counts media spend and conversions, then ignores the creative freelancer, the email tool, the agency retainer, the salary of the person managing campaigns, and the pile of small software costs that keep acquisition running.

A clean-looking CPA can hide an ugly acquisition model.

Used properly, cost per acquisition is one of the sharpest decision tools in a DTC business. It helps you decide which channel deserves more budget, which offer needs work, when a campaign is lying to you, and whether your growth is real or just expensive. Used badly, it encourages you to scale the wrong thing faster.

This is the version that matters in practice. Not the glossary definition. Not the dashboard screenshot. The version that tells you whether each new customer strengthens the business or weakens it.

#Table of Contents

- Introduction

- What Cost Per Acquisition Really Means

- How to Calculate Your True CPA

- What Is a Good CPA for a DTC Brand

- Common CPA Measurement and Attribution Issues

- How to Lower Your Cost Per Acquisition

- Putting Your CPA to Work

#Introduction

You pull up Ads Manager on Monday morning. Meta says your CPA is healthy. Google looks acceptable too. Then you check the P&L and wonder why cash feels tighter than the dashboards suggest.

That gap is where a lot of DTC brands get into trouble.

Founders usually do not lose money because they forgot the CPA formula. They lose money because they track a vanity CPA that captures media spend and ignores the rest of the work required to get a customer through the door. Creative production, agency fees, freelancers, retention discounts used to close the first order, landing page tools, and the team running the machine all count. Your ad platform does not carry that burden. Your business does.

So the critical question is not just, “What did the platform report?” It is, what did it cost to acquire this customer in a way that leaves margin left over?

Benchmarks can give you rough context, but they are easy to misuse. Analysts at Flipkart Commerce Cloud's overview of cost per acquisition note that average e-commerce CPA can fall anywhere from $20 to $65 globally, and in the U.S. can range from $21 to more than $300 depending on category and competition. Useful? A little. Actionable on their own? Not much. A skincare brand with strong repeat purchase behavior can survive a CPA that would wreck a one-and-done gadget brand.

A simple example shows why the surface-level number can be misleading. If a campaign spends $5,000 and generates 250 purchases, the standard CPA formula gives you $20. The math is clean. The business reality often is not. Add the designer who made the ads, the agency retainer, the post-purchase discount that trained conversion, and the app stack supporting the funnel, and that “good” CPA can stop looking good fast.

Practical rule: The only CPA worth trusting is the one that still leaves room for contribution margin after the hidden costs are included.

Brands that use CPA well treat it as an operating number, not a vanity metric. They use it to decide how hard to scale, which channels deserve more budget, and when reported efficiency is just accounting fiction.

#What Cost Per Acquisition Really Means

A founder looks at Meta, sees a $22 CPA, and decides to scale. Two weeks later, margin is tighter, cash is gone faster, and the ad account still says performance is fine. That usually means the brand was tracking a vanity CPA, not the actual cost of acquiring a customer.

#The simple formula and the trap inside it

At its simplest, cost per acquisition is:

total campaign cost ÷ number of acquisitions

In an ad platform, that usually means media spend divided by attributed purchases. Useful? Yes. Complete? Usually not.

Platform CPA is a channel metric. It tells you what the ad account spent to produce conversions under that platform's rules. Your P&L cares about something else. It cares what it took in total to win that customer after the creative, people, tools, and outside help are counted.

That gap is not small. Failing to separate “true CPA” from media-only CPA can lead to a 30–50% underestimation of acquisition costs, according to Umbrex's CPA analysis guide.

That is how brands convince themselves a channel works when it only works on a dashboard.

I see the same miss over and over. A team reports a healthy CPA from paid social, but the result depends on a freelance editor, a retention tool keeping conversion rates up, a founder spending hours reviewing creative, and an agency fee sitting in another spreadsheet. Strip those costs out and the number looks clean. Put them back in and you get the number you can actually run the business on. Good ecommerce analytics discipline closes that gap before it turns into bad budget decisions.

If your CPA works only after you ignore the costs around the ad spend, it is a reporting artifact, not an operating metric.

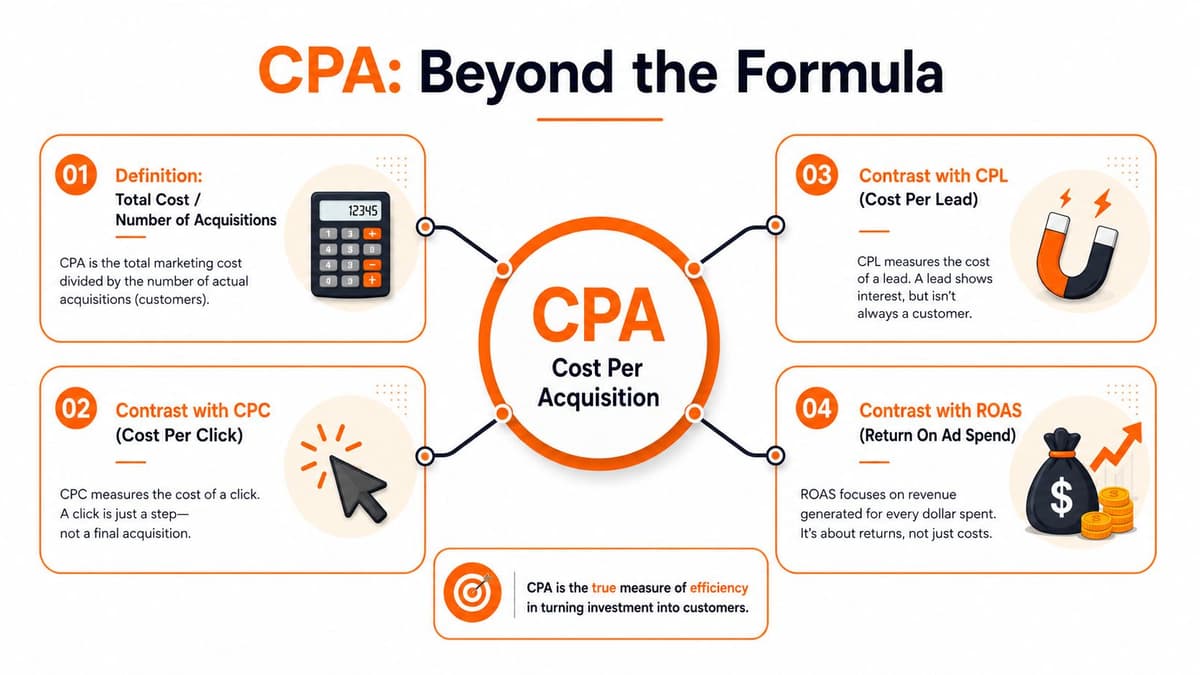

#CPA versus CAC and ROAS

Founders blur CPA, CAC, and ROAS because all three show up in the same reports. They answer different questions.

A coffee shop promotion makes the distinction clear:

- CPA is the cost to get one person to buy from a specific campaign

- CAC is the full cost of sales and marketing divided by new customers

- ROAS is the revenue generated relative to ad spend

The practical mistake is using one metric to do another metric's job.

Use CPA to judge whether a campaign or channel is buying customers efficiently. Use CAC to judge whether the business can afford its current growth model. Use ROAS to add revenue context, then sanity-check it against margin and repeat purchase behavior.

ROAS causes the most damage in DTC when founders treat it like a profit metric. A campaign can post strong revenue return and still bring in discount-heavy customers, low-AOV orders, or one-time buyers who never cover acquisition cost. A low-looking CPA can mislead you too if it excludes the operating costs behind the campaign.

The point is simple. CPA only becomes useful when you know which version you are looking at. Media CPA helps with channel management. True CPA helps you decide whether scaling will make you more money or just spend it faster.

#How to Calculate Your True CPA

A founder looks at Meta, sees a $22 CPA, and decides to scale. Thirty days later, cash is tighter, not better. The ad account was not lying. The math was incomplete.

That is the trap. Plenty of brands track a vanity CPA that includes media spend and ignores the costs required to produce, manage, and convert that traffic. If you want CPA to help you make money, calculate it in layers.

#Start with media CPA

Media CPA is the fast read. You need it by platform, campaign, ad set, and creative angle because it shows where efficiency is slipping.

The formula is simple:

media spend ÷ attributed conversions

Use that number to manage buying decisions inside the ad account. If one campaign is paying far more for the same outcome, cut it, fix it, or cap it.

Keep the role of this metric narrow. Media CPA is useful for channel management. It is a weak operating metric on its own.

#Build the fully loaded version

A full customer acquisition cost includes ad spend, salaries, tools, creative production, and agency fees, divided by new customers acquired, according to Geckoboard's CAC definition. That is much closer to a true CPA you can use for budgeting and scaling.

Founders often deceive themselves. They count the spend that is easy to export and ignore the spend that sits in payroll, freelancers, software, and production. The result looks efficient in a dashboard and mediocre in the bank account.

The missed costs are usually predictable:

- Creative costs. Product shoots, UGC editing, designers, video freelancers.

- People costs. The marketer running Meta, the founder's time if they still manage campaigns, contractors, and agencies.

- Tooling costs. Klaviyo, Triple Whale, heatmap tools, landing page builders, reporting tools.

- Conversion support costs. Copywriting, landing page design, CRO help, promo setup.

- Channel-specific extras. Affiliate management fees, sampling, marketplace fees, or other costs tied directly to acquisition.

Track CPA in three layers:

- Media CPA

Ad spend divided by attributed conversions. - Channel-loaded CPA

Media CPA plus the direct costs required to run that channel. - True acquisition CPA

Channel-loaded CPA plus the broader sales and marketing overhead tied to winning new customers.

That layered view prevents bad decisions. A paid social campaign can look cheap in-platform and turn ugly once creative churn and management costs are included. Another can look expensive on media CPA and still make sense if the channel brings in stronger customers and needs less support to convert.

#Sample True CPA calculation template

Build this in a spreadsheet and update it monthly. Teams that want cleaner reporting and fewer attribution arguments should pair this with a tighter ecommerce analytics operating rhythm.

| Cost Component | Example Monthly Cost | Your Monthly Cost |

|---|---|---|

| Ad spend | $5,000 | |

| Creative production | ||

| Agency or contractor fees | ||

| Marketing software and tools | ||

| Marketing team salaries allocated to acquisition | ||

| Landing page and CRO support | ||

| Total acquisition cost | ||

| New customers acquired | 250 | |

| Media CPA | $20 | |

| True CPA |

The math in that example is straightforward. $5,000 in spend divided by 250 purchases gives you a $20 media CPA. Useful, but incomplete. A more complete calculation starts when you add the costs that made those 250 purchases possible.

Operator's habit: Track this by channel, not just in aggregate. Aggregate CPA can hide one strong channel subsidizing two weak ones.

Update true CPA at least monthly. Paid channels with enough volume should be reviewed weekly so you can catch rising costs before they turn into a scaling mistake.

#What Is a Good CPA for a DTC Brand

#Benchmarks are useful but limited

Founders always ask the same question first: what's a good CPA?

The honest answer is that benchmarks can orient you, but they won't save you.

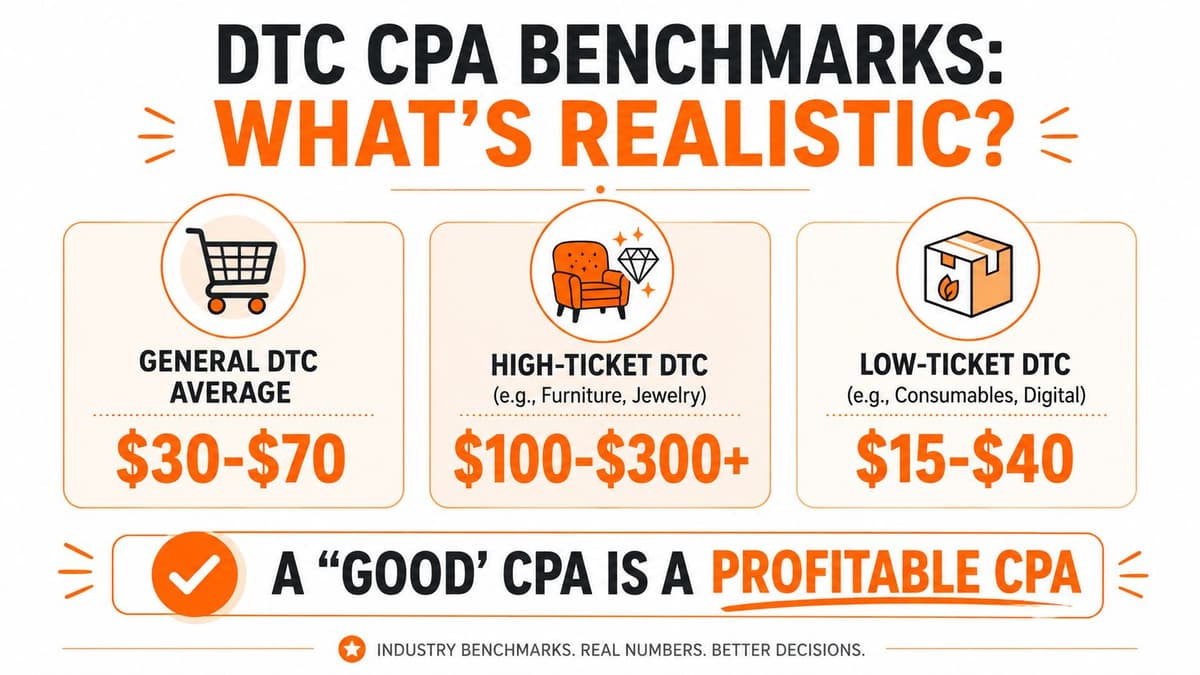

Across the global e-commerce sector, average acquisition cost typically falls between $20 and $65, according to Flipkart Commerce Cloud. Other e-commerce benchmark references place average customer acquisition costs around $70, with ranges from $53 on the low end to over $90 on the high end, including $64 for advertising specialty and promotional brands in Rivo's ecommerce CAC benchmark summary. Geckoboard's CPA benchmark page also notes a typical e-commerce CPA range of $50–$150.

Those numbers are useful for one reason. They tell you whether your CPA is roughly normal, suspiciously low, or alarmingly high for the type of selling you're doing.

They do not tell you whether your business can afford it.

#The ratio that actually matters

The better question is this: what CPA can your business support profitably?

That's where LTV:CPA matters more than a benchmark. A profitable ratio is approximately 3:1, meaning every $1 spent on acquisition should generate $3 in lifetime revenue, according to Triple Whale's guidance on a good CPA. The same reference says 2:1 or less is a warning sign.

That changes how you read performance:

- A low CPA can still be bad if the customers are low value, discount-sensitive, or one-and-done.

- A higher CPA can be fine if repeat purchase behavior is strong and margins hold.

- An extremely efficient CPA can also be a problem if it means you're underinvesting and leaving growth on the table.

A useful test is to compare CPA with your average order value and retention profile. Triple Whale also notes that if CPA rises above 30–40% of AOV without strong retention, profitability erodes in many e-commerce cases, in its same benchmark discussion.

If you're trying to acquire net-new customers for a repeat-purchase brand, your target CPA should reflect what happens after order one. If you're selling a low-repeat, lower-margin product, your tolerance should be tighter. This is why comparing your brand to a random DTC thread online is usually useless.

For teams trying to improve this systematically, the key insight is tying acquisition reporting to customer value, not just ad efficiency. That's the difference between buying orders and building a durable new account acquisition strategy.

#Common CPA Measurement and Attribution Issues

A founder looks at Meta and sees a $38 CPA. Google shows $42. Shopify says the orders came through direct and branded search. The team celebrates efficient acquisition, then wonders why contribution margin still looks soft at the end of the month.

That gap usually comes from measuring a vanity CPA instead of a true one.

#Why platform CPA often disagrees with reality

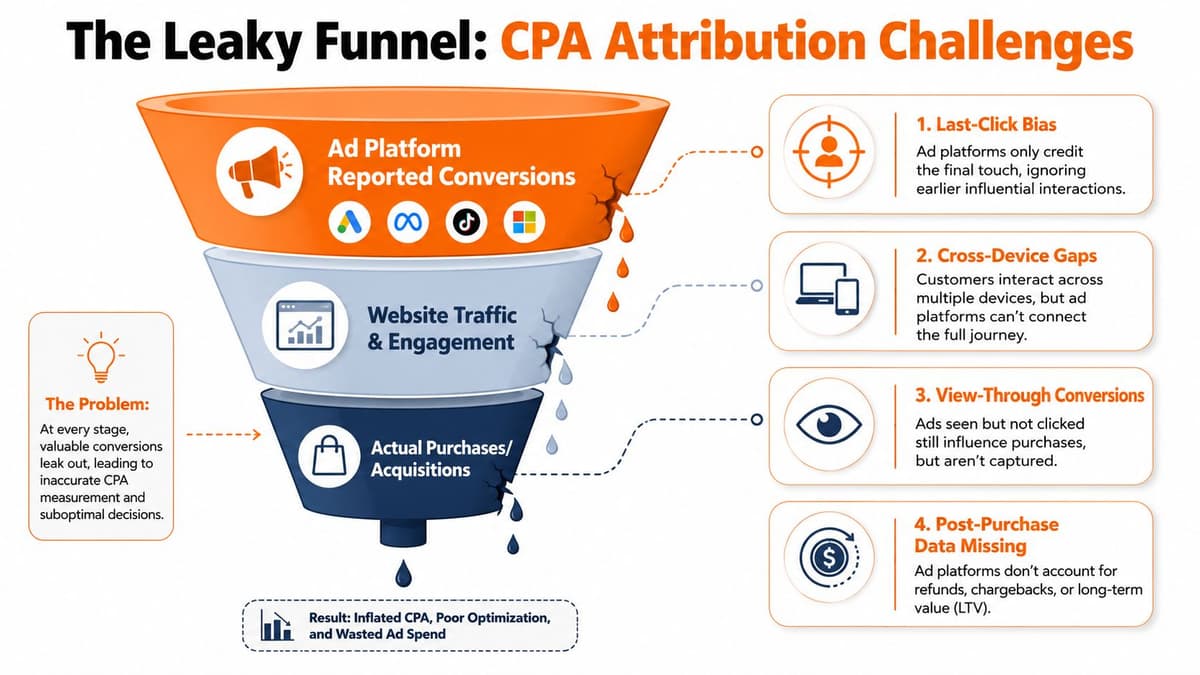

Each system is answering a different question. Ad platforms report the conversions they can claim. Your store reports the session that closed the sale. Your finance view cares about what it cost to get a paying customer who keeps the order.

One order can be credited three different ways without anyone technically lying. Meta may claim the click that introduced the product. Google may claim the branded search that captured existing demand. Shopify may log the final session. Your P&L counts one customer.

Channel comparisons get distorted fast if you ignore intent. Search often captures demand that already exists. Display and paid social often create that demand earlier. If both channels touch the same buyer, lazy attribution makes the closer look brilliant and the introducer look inefficient. That is how founders cut prospecting, protect branded search, and slowly choke future growth.

#Where double counting sneaks in

Three failure patterns show up over and over.

- Last-click bias. The channel nearest to checkout gets too much credit. Branded search and email often inherit demand created somewhere else.

- View-through inflation. A platform counts a conversion after an impression without a click. That can be useful as directional data, but it is dangerous as a budgeting number.

- Cross-device gaps. A shopper sees the ad on mobile, buys later on desktop, and the path breaks across tools.

This short walkthrough is worth watching if you want a visual explanation of how attribution distorts acquisition reporting:

There's another issue founders miss. Platforms optimize toward the conversion event they can see. They do not care whether that customer refunds, uses a steep discount, buys once and disappears, or costs more to service than expected. A reported CPA can look healthy while your true CPA is already upside down.

#How to sanity check attribution

Perfect attribution is not the goal. Better budget decisions are.

Use a few checks that make inflated CPA reporting easier to spot:

- Compare platform conversions to store-level new customer counts. If ad managers show strong acquisition but net-new customers are flat, credit is being overstated somewhere.

- Split prospecting and retargeting. Blending them hides the actual cost of generating fresh demand.

- Review first-order customers by source, not just orders. Repeat purchases and returning traffic can make weak acquisition look stronger than it is.

- Check assisted paths before shifting budget. A multi-touch attribution model will not solve every blind spot, but it gives far less credit to the final touch by default.

- Match acquisition data with post-purchase quality. Refund rate, second-order rate, and discounted order mix all belong in the same CPA review.

The practical rule is simple. If a channel reports a great CPA but fails the new-customer, margin, or retention check, treat that number as advertising math, not operating truth.

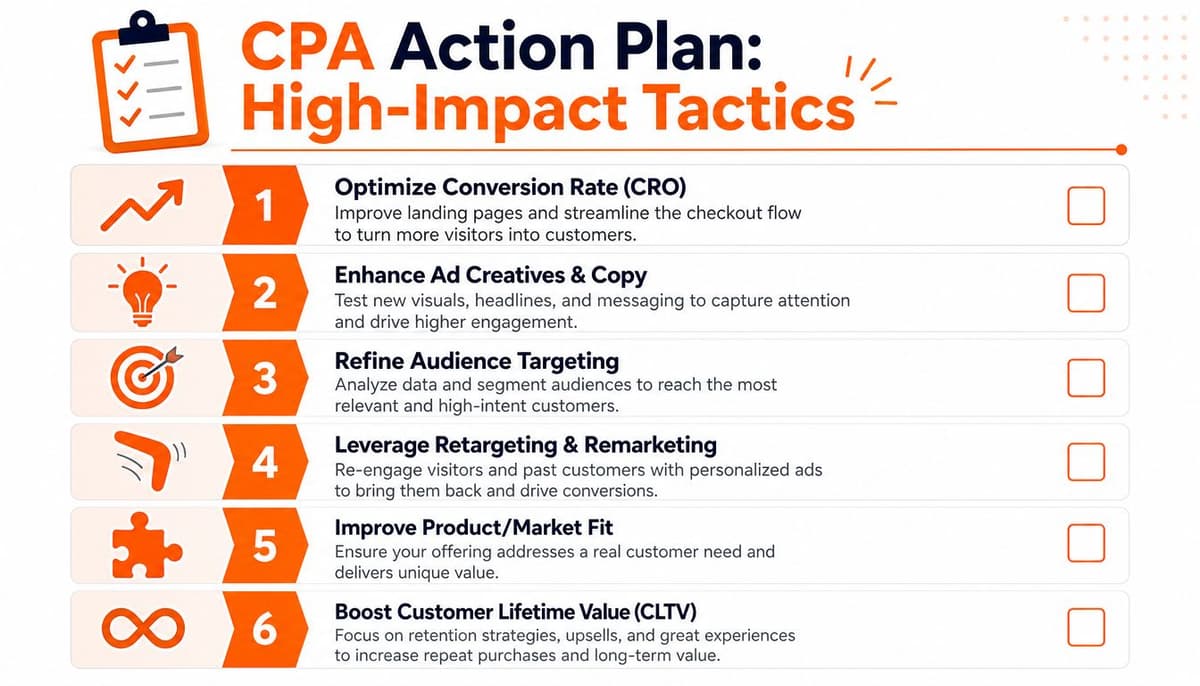

#How to Lower Your Cost Per Acquisition

You launch a new ad set, platform CPA looks fine, and the week still ends with less cash than expected. That usually means the problem is not one setting. It is that the business is measuring and improving the wrong CPA.

Lowering CPA starts with the number you are trying to lower. If you chase a vanity CPA that excludes creative costs, agency fees, discount-heavy orders, or poor first-order quality, you can make the dashboard look better while profit gets worse. The goal is not a cheaper reported conversion. The goal is to acquire profitable customers at a cost the business can support.

A useful guardrail helps here. The U.S. Small Business Administration guidance summarized by Recharge suggests many ecommerce businesses spend around 7 to 8 percent of revenue on marketing as a general benchmark, not a universal rule, according to Recharge's summary of ecommerce acquisition costs. Treat that as a reasonableness check. If your spend is above that level and first-order economics still look weak, buying more traffic usually makes the problem bigger.

#Fix the biggest leaks first

Founders often start with bids because bids feel controllable. In practice, CPA usually drops faster when you fix the parts customers experience: the ad, the offer, and the page they hit after the click.

Start with this order:

- Creative

- Offer

- Landing page

- Audience structure

- Post-purchase economics

That sequence matters. A weak ad sent to the perfect audience is still a weak ad. A strong ad that lands on a confusing PDP still burns cash. And a good first purchase from a customer who never buys again can still be an expensive mistake.

#High impact work inside the ad account

#Creative usually moves CPA more than account tinkering

Many brands spend too much time reorganizing campaigns and too little time improving what the customer sees. Creative fatigue, weak hooks, unclear product benefits, and generic proof can push CPA up fast.

Better creative does a few things well:

- Calls out a specific problem

- Shows the product in use

- Gives the shopper a reason to believe

- Matches the awareness level of the audience

- Sets up the landing page instead of contradicting it

If I had to pick one place to look first when CPA rises, it would usually be the ads customers have seen too many times. Founders keep trying to squeeze efficiency out of tired creative because replacing it takes work. That is expensive procrastination.

#Tighten message to audience fit

Broad targeting can work. It works best when the product is easy to understand and the creative does the filtering. It works badly when the product needs context, comparison, or education.

Different buyers respond to different reasons to purchase. Gift buyers need a different angle than replenishment shoppers. Problem-aware shoppers need a different message than people who have never heard of the category. If you run the same promise to all of them, CPA climbs because too many paid clicks arrive half-qualified.

Practical fixes:

- Separate prospecting from remarketing

- Split creative by buying intent

- Exclude existing customers from new customer campaigns when possible

- Cut audience and ad combinations that spend without finding first-time buyers

One simple test catches a lot of waste. Read the ad headline, then read the first screen of the landing page. If they feel like two different conversations, expect CPA to rise.

#Medium impact work on the site

Paid traffic makes site problems more expensive. Every bit of friction on the path to purchase turns media spend into bounce rate.

Review the page like a skeptical first-time customer. Is the product clear in five seconds? Is pricing obvious? Are shipping and returns easy to find? Is the mobile page fast and readable? Does the PDP answer the objections a new shopper has, or does it just list features?

The common leaks are boring, but they are expensive:

- Slow mobile load times

- Weak product page hierarchy

- Hidden shipping costs

- Too many checkout fields

- Discount popups that interrupt purchase intent

- Trust signals buried too far down the page

Founders also hurt CPA by optimizing for prettier metrics instead of better economics. A popup can raise email capture and still reduce purchase rate. A deeper first-order discount can improve conversion rate and still wreck contribution margin. The right question is simple: did this change reduce the cost of acquiring a profitable customer?

#Improve the offer before forcing more spend

Some CPA problems are really offer problems.

If traffic is reaching the site and failing to convert, the market may be telling you the product framing is weak, the bundle is wrong, the price-to-value story is unclear, or the first-order incentive is poorly structured. Founders often call this a targeting issue because changing targeting feels easier than changing the offer.

A stronger offer does not always mean a bigger discount. In many DTC categories, it means clearer value. Better bundles. A stronger guarantee. More useful proof. Better product education. A gift-with-purchase can outperform a percentage discount if it protects margin and improves perceived value.

#Lower true CPA by improving customer quality

Some brands should lower CPA. Others should increase what each acquired customer is worth.

The vanity CPA trap becomes expensive. A channel can produce a low reported CPA by pulling in discount buyers who refund more, churn faster, or never place a second order. Another channel can look worse on day one and win over 90 days because the customers stick.

Ways to improve customer quality after the first purchase:

- Build welcome and post-purchase flows that drive order two

- Use replenishment reminders where the product has a natural repeat cycle

- Merchandise the next best product instead of pushing blanket discounts

- Review retention by source so you know which channels buy real customers, not cheap ones

If your post-purchase system is weak, every acquisition channel has to work harder. If your retention system is strong, the business can tolerate a higher CPA without breaking.

#A practical monthly CPA review

Run this once a month and force the numbers to answer hard questions.

- Recalculate true CPA with media, creative production, tools, salaries, agency spend, and discounts that materially affect margin

- Review CPA by channel and by net-new customer contribution

- Check whether top-spend campaigns are bringing in customers who repurchase, not just customers who convert once

- Pause tired creative before performance falls off a cliff

- Match every major ad angle to a relevant landing page

- Audit checkout friction on mobile

- Look at refund rate and discounted order mix by acquisition source

- Compare total marketing spend against your revenue and margin structure using the SBA benchmark summarized earlier, rather than treating platform CPA as the whole story

- Protect retention work, because a weak second-order system inflates true CPA

Lower CPA is useful only if it improves profit. The founder move is not chasing the cheapest customer on paper. It is cutting waste, fixing conversion leaks, and building a business that can afford growth because the CPA you track is the accurate one.

#Putting Your CPA to Work

Cost per acquisition becomes powerful when you stop treating it like a scoreboard. It's a decision tool. It tells you where to cut, where to lean in, and where the numbers in your ad account are flattering a broken system.

The useful version is the honest one. Calculate the fully loaded number. Judge it against customer value, not vanity benchmarks. Challenge attribution before trusting it. Then use that information to reallocate budget, sharpen creative, fix site friction, and strengthen retention.

Founders who do this consistently don't just buy customers more efficiently. They build a business that can scale without lying to itself.

Arlo helps Shopify brands turn messy store data into decisions you can act on fast. If you want a clearer read on acquisition efficiency, wasted ad spend, conversion leaks, and retention opportunities without living in five dashboards, Arlo delivers a concise weekly analysis that shows what changed, why it matters, and what to do next.